VA HOME LOAN ACADEMY

Helping Veterans understand the home loan benefit they’ve earned.

Straightforward guidance from John Walowac for Veterans, active duty service members, military families, and realtors navigating a VA home loan in VA, MD, DC and WV.

Welcome to the VA Home Loan Academy

If you’ve served our country, first, thank you.

One of the things I’ve enjoyed most throughout my career is helping Veterans and military families become homeowners. I’ve found that many of the Veterans I work with share some the the same qualities – they’re dedicated, organized, thoughtful planners, and they take pride in doing things the right way. I have a tremendous amount of respect for that.

For me, helping Veterans use one of the benefits they’ve earned is my own small way of giving back to the people who have given so much in service to our country.

Over the years, I’ve also noticed something else.

Veterans – and even many experienced Realtors – have a lot of questions about VA home loans. Some people think they need a large down payment. Others believe they can only use their VA loan once. I’ve talked with Veterans who assumed they didn’t qualify, or who believed buying a home simply wasn’t affordable to them anymore.

Unfortunately, there’s a lot of misinformation out there.

Our Promise

You’ll never be pressured to apply for a mortgage just because you visited the Academy. My goal is simple: to help Veterans understand the home loan benefit they’ve earned so they can make confident decisions—whether they’re ready to buy today or years from now.

Why I Created The VA Home Loan Academy

The VA home loan is one of the strongest mortgage benefits available, but many eligible Veterans never take full advantage of it because they don’t fully understand how it works. My hope is that this Academy changes that.

I created the VA Home Loan Academy to answer questions I hear every week from Veterans, homeowners, and Realtors. My goal is to explain VA loans in plain English – not mortgage jargon – so you can understand your options and make informed decisions with confidence.

One thing you’ll notice throughout these lessons is that I spend a lot of time talking about numbers. That’s intentional.

I believe education comes before the mortgage.

One of the most valuable tools I use with my clients is something called a Total Cost Analysis. Instead of showing just one loan option, we compare different scenarios side by side. We look at monthly payments, cash needed at closing, long-term costs, and how each option fits your financial goals.

Sometimes the best solution isn’t the one people expect.

When you can clearly see the numbers, you can make decisions based on factos instead of assumptions.

Whether you’re buying your first home, moving up to a larger home, refinancing, or simply wondering if you’re eligible to use your VA benefit, my goal is never to pressure you into making a decision. It’s to help you understand your options so you can move forward knowing you’ve made the choice that’s right for you and your family.

I hope these lessons answer your questions, clear up some common misconceptions, and give you the confidence to take the next step whenever you’re ready.

Thanks for visiting the VA Home Loan Academy. I’m honored you’re here and I look forward to helping you make the most of the home loan benefit you’ve earned.

What You’ll Learn

Lesson 1

What Are The Rules for a VA Home Loan?

Eligibility, occupancy, down payment, property rules and common myths.

Lesson 2

Who Pays Closing Costs on a VA Loan?

What Veterans can pay, what sellers can cover, and what to expect.

Lesson 3

VA Loan vs Conventional Loan

When VA is stronger – and when another option might make sense.

Lesson 4

How Much Income Do I Need?

A $500,000 home example using real payment factors.

Lesson 5

Biggest VA Loan Myths

The rumors that keep Veterans from using their benefits.

Lesson 6

Can I Use My VA Loan Benefit More Than Once?

Entitlement, restoration, and move up buyer strategy.

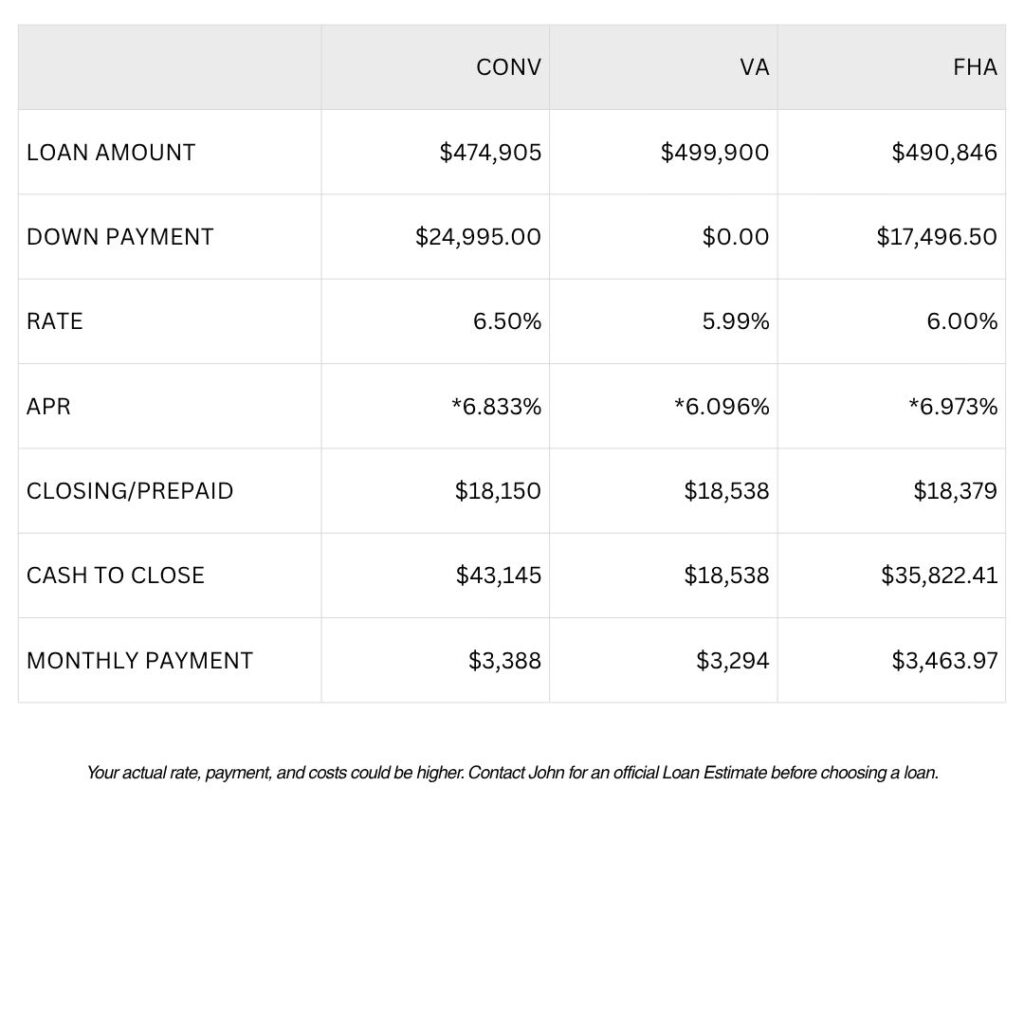

John’s Total Cost Analysis

VA loan choices are not always one-size-fits-all. John compares monthly payment, cash to close, long term costs, refinance opportunities, and what each option means for your goals.

Home loans are structured based on many factors and are different for each person. John takes a look at credit history, income, assets, debt obligations, occupancy requirements and property eligibility to show you your best options.

Sample Scenario

Why Veterans Work With John

- Explains every option in plan English

- Creates Total Cost Analysis comparisons

- Works with first-time buyers and move-up buyers

- Licensed in Virginia, Maryland, Washington DC and West Virginia

- Continues helping after closing with refinance planning

Ready to Talk?

Whether you’re buying your first home, moving to a new duty station, or wondering if refinancing makes sense, I’m happy to answer your questions. Even if you’re just exploring your options, let’s start with a conversation.

This article is provided for educational purposes only and should not be considered legal, tax or financial advice. VA home loan eligibility is determined by the US Department of Veterans Affairs, while loan approval is subject to lender underwriting requirements. Eligibility, funding fees, loan limits, interest rates, and program guidelines may change without notice.

Not all applicants will qualify. Loan approval depends on factors including credit history, income, assets, debt obligations, occupancy requirements, and property eligibility.

VA loans are available to eligible Veterans, active duty service members, certain members of the National Guard and Reserve, and qualified surviving spouses. A Certificate of Eligibility (COE) may be required.

If you’re wondering how these guidelines apply to your situation, I’m happy to walk through your options and help you determine the best path forward.